Intended Value vs FMV: should you care?

We get hung up on the difference while paying little attention to a far more impactful valuation alternative.

When the Comp Committee approves an RSU grant, the number of shares is typically based on an intended value divided by a price formula, such as the 20-trading-day average closing price. But when the grant is recorded, the fair market value (“FMV”) reflects the closing price that day.

As a result, the intended value set by the compensation team varies from the fair market value recorded.

Should you care?

Most comp leaders would say yes — we should stick to intended value because that methodology aligns with how we set targets.

But how much does it really vary, and when does it matter?

I experimented with analyzing stock data from 10 public companies to find out. And the answer is, as every consultant says, it depends:

SBC expense and RSU budgets — yes, you should care, especially for the annual refresh grants

Employee expectations — yes, if your stock is highly volatile

Market data methodology — no, the variance is de minimis

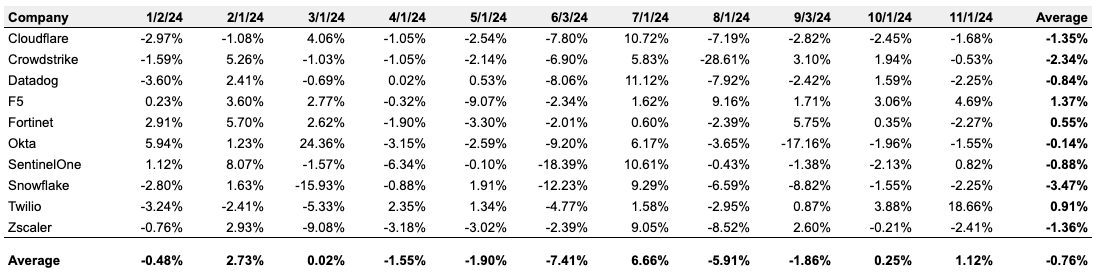

Analysis of 10 companies in 2024 YTD

I looked at 10 tech companies in the data security industry to see how big the gap gets:

Cloudflare, Crowdstrike, Datadog, F5, Fortinet, Okta, SentinelOne, Snowflake, Twilio, and ZScaler

I picked this group of stocks because they were highly volatile in 2024, maximizing differences between FMV and intended value:

Using historical stock price data from NASDAQ, I built an analysis of year-to-date (through November 20th) variance in the 20-day average closing price (Intended) and actual closing price (FMV) for each company, then assumed a grant date on the start of each month.

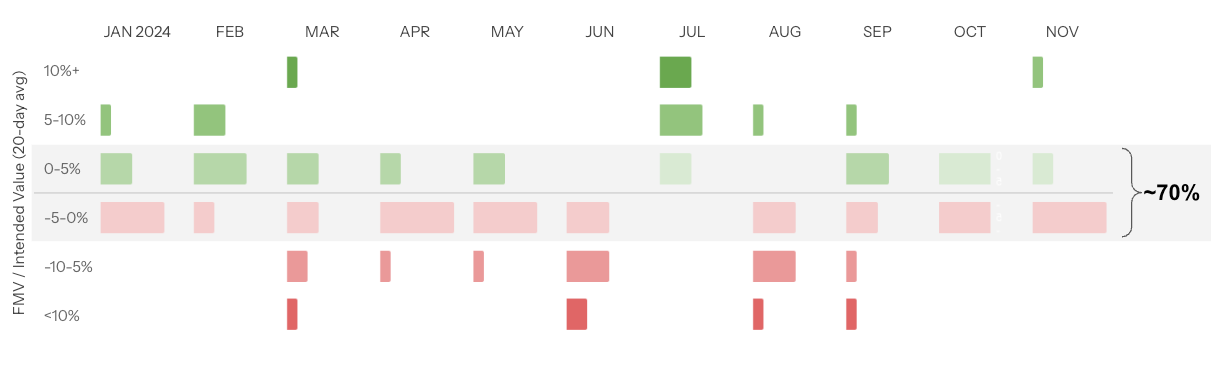

Here are the results:

This analysis shows that most of the time the variance between FMV and intended value was minimal — 70% of all observations were less than +/-5%.

The average variance for all events was -0.76%, and in absolute terms was 4.50%.

But in any given month, the difference can get pretty big, like Snowflake at -15.93% in March, or Twilio at 18.66% in November. 7 out of 10 companies had at least one grant date month where the difference was greater than 10%.

So does this variance between fair market value and intended value matter for comp?

Let’s start by looking at everyone’s favorite topic right now: SBC expense.

SBC expense and RSU budgets — you should care

If your stock has a big swing before you make a large set of grants, like getting your annual refresh grants approved, then FMV versus intended value can cause big headaches.

For an illustrative example, take Okta — imagine they granted their refresh grants on March 1, 2024, when the 20-day average closing price was $87.24 and the fair market value price was $108.49.

This is a windfall for employees (more on that later), but it’s a problem for the CFO.

Let’s say they intended to spend $150 million that day, an average refresh grant of about $25k for their 6,000 employees. Since the FMV was 24% higher, their SBC expense recognized over the total vesting period will reflect closer to $186 million, for a difference of +$36 million. 😱

Notice the stock volatility impacts your RSU budget and share dilution, too. In this illustrative example, sticking with the 20-day average closing price results in spending 1.72 million shares, whereas the FMV implies spending 1.38 million shares, 20% fewer.

Philosophical aside: if the gap between a 20-day average closing price and the FMV is big — which methodology do you think more closely reflects “intended” value?

If I’m spending an extra $36 million in SBC expense and an extra 340,000 shares, I hope I’m doing it intentionally…

So if you have a big list of grant approvals at your next Comp Committee meeting and your stock price has shot up in the last month, you better have a conversation with your CFO first.

Employee expectations — yes, it matters

If your stock price suddenly changes, employees can get a big windfall (or haircut) on the day of the grant.

For example, if you joined Crowdstrike in August, you might be a little annoyed: the stock dropped 43% over the previous 20 trading days, resulting in a FMV 28.6% lower than the 20-day trading average. Meaning, if you were promised a $100k new hire grant in your offer letter, you got 318 RSUs now worth only $71k.

Whether your comp team wants to remediate that unlucky timing is a question of compensation philosophy and talent strategy. But every team should at least be prepared for a surge of complaints from unhappy employees who received a fraction of what they expected, despite the language they signed in their offer letter.

Can’t help myself — gotta raise my philosophical aside again: if the gap between 20-day average and FMV results in a 29% haircut for employees that month… which valuation feels more “intended”?

Market data methodology — not much 🤷

For individual companies and specific grants, FMV versus intended value can vary meaningfully when your stock price is volatile.

But in aggregate, it appears de minimis.

The average FMV/Intended variance across these 10 companies’ 2024 grant dates is 4.50% in absolute terms, but it washes out to -0.76% taking into account positive and negative swings.

That’s a rounding error.

Consider the variance compared to the difference in market percentile for a P4 software engineer:

50th percentile new hire grant is $300k

75th percentile is $450k

A grant 4.5% higher than the median interpolates to the 52nd percentile

50th versus 52nd percentile is pretty uninteresting.

Target vs actual — the real conversation

I get why we want to use intended value for stock comp benchmarking:

It reflects target value, paralleling construction with target bonus so we can build up to a target TDC

It reflects policy when we use market data to construct ranges

We’re used to getting our data this way, and it needs to be apples-to-apples

But the real conversation about stock comp is the actual value the employee experiences: realized value and current unvested value.

Realized value: the vested amount that shows up on your W2 — am I making more money this year than last year?

Current unvested value: the value of all unvested shares at today’s price — do I have more unvested stock than what I could get by moving to a competitor?

Whether an employee feels valued and whether you’re protected against attrition are the outcomes of your compensation strategy. I think most comp teams give this far too little attention, mostly because it’s historically been hard to analyze.

FMV, on the other hand, appears to be such a close proxy for intended value that focusing concern here often feels pedantic.

Peer Group is a newsletter for comp leaders navigating market volatility in the new era of pay transparency! If you want to share my newsletter, you can forward this email to your colleagues and fellow comp leaders.

Want more polls and insights about today’s volatile talent markets?

Subscribe by hitting the button below.